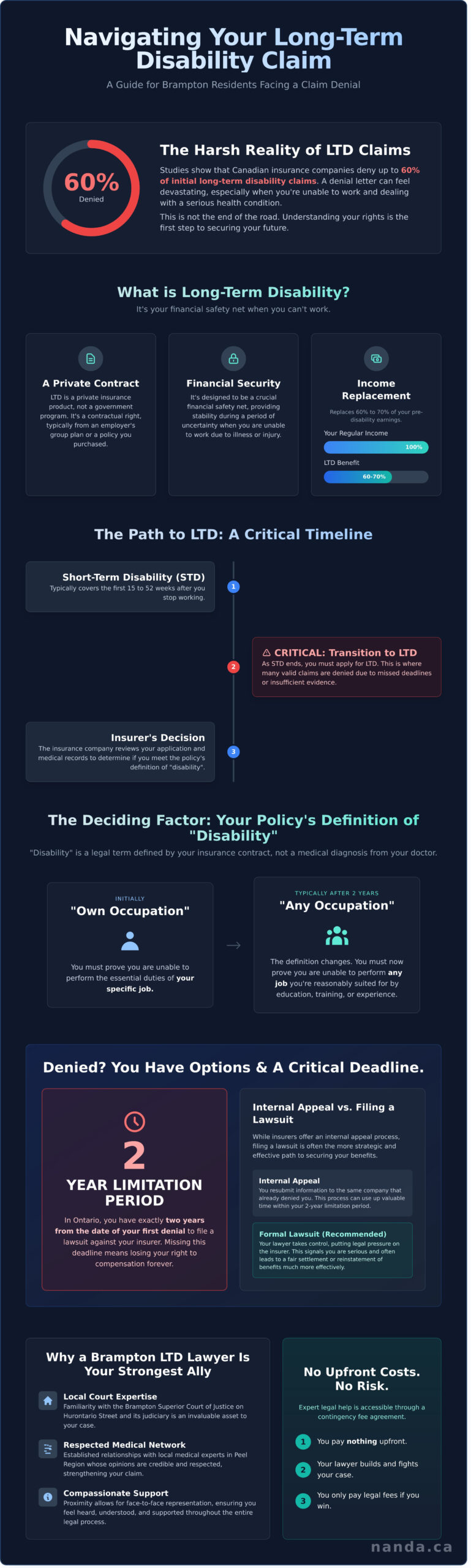

Did you know that some studies show Canadian insurance companies deny as many as 60% of initial long-term disability claims? When you’re unable to work due to a serious illness or injury, a denial letter can feel like a final, devastating blow. The complex language in insurance policies and the pressure of looming deadlines only add to the immense stress, especially when you’re dealing with an ‘invisible’ disability that others may not understand. It’s a frustrating and isolating experience, but it is not the end of the road.

This guide is designed to restore your sense of control. We will walk you through the essential steps of the LTD claims process, explain your rights under Ontario law, and show how partnering with a dedicated long term disability lawyer Brampton can be the most critical decision in securing your financial future. We’ll cover everything from deciphering your policy and meeting critical deadlines to building a compelling appeal for the reinstatement of your benefits or a fair lump-sum settlement, giving you the peace of mind you deserve.

Key Takeaways

-

Understand that "disability" is a legal term defined by your insurance policy, not just a medical diagnosis from your doctor.

-

Identify the common reasons insurers deny LTD claims and learn why a formal lawsuit may be more strategic than an internal appeal.

-

Recognize the critical 2-year limitation period in Ontario for taking legal action after a claim denial to protect your rights to compensation.

-

Learn how contingency fee agreements make it possible to hire an expert long term disability lawyer brampton with no upfront costs.

Table of Contents

Understanding Long-Term Disability (LTD) in Brampton

When a serious illness or injury prevents you from working, the financial and emotional stress can be overwhelming. Long-Term Disability (LTD) benefits are designed to be a crucial financial safety net, providing income replacement when you need it most. These benefits are a contractual right, typically part of a group insurance plan provided by your employer or a private policy you’ve purchased yourself. It’s not a government program, but a private insurance product meant to protect your financial stability.

Most disability claims begin with Short-Term Disability (STD), which usually covers a period of 15 to 52 weeks. As this period ends, if your condition still prevents you from returning to work, you must apply for LTD. This transition is a critical point where many valid claims are unfortunately denied. A foundational understanding Long-Term Disability (LTD) is the first step toward securing the benefits you are owed.

Key Takeaways for LTD Claims

-

Eligibility Defined: To qualify for LTD, you must provide comprehensive medical evidence proving that your disability prevents you from performing the essential duties of your "own occupation" (initially) and later, any occupation for which you are reasonably suited.

-

Critical Timelines: The application process from STD to LTD is time-sensitive. Missing a deadline can jeopardize your entire claim, making prompt action essential.

-

The Role of Legal Counsel: An experienced lawyer protects your rights, manages communication with the insurer, and builds a robust case to prevent wrongful denials or premature termination of benefits.

Please note: The information provided in this article is for general informational purposes only and does not constitute legal advice. You should contact a qualified professional for advice on your specific situation.

The Role of LTD as a Financial Safety Net

LTD policies are structured to replace a significant portion of your income, typically providing between 60% and 70% of your regular pre-disability earnings. In a city like Brampton, with its diverse economic landscape of industrial, logistics, and professional workforces, this income is vital for maintaining your family’s quality of life. Whether you work in a manufacturing plant near the 410, a corporate office, or a healthcare facility like Brampton Civic Hospital, your LTD policy serves the same purpose: to provide stability during a period of uncertainty. Group insurance policies offered by employers are most common, but individual policies offer another layer of protection, especially for self-employed professionals.

Why a Brampton-Based Legal Perspective Matters

When your claim is denied, you need a legal team that understands the local landscape. Our lawyers have extensive experience advocating for clients at the Ontario Superior Court of Justice in Brampton, located right on Hurontario Street. This familiarity with the local judiciary is invaluable. Furthermore, a successful claim depends on strong medical evidence. An effective long term disability lawyer Brampton residents can rely on will have established relationships with local medical experts in Peel Region whose opinions are respected. This expertise is something a personal injury lawyer also cultivates, as they too rely on credible medical documentation. Proximity allows us to offer compassionate, face-to-face representation, ensuring you feel heard and supported throughout your case.

Legal Definitions: How Ontario Law Determines Disability

When you file for long-term disability, the most critical word isn’t your diagnosis; it’s the definition of "disability" itself. This isn’t a medical term but a legal one, strictly defined by the specific language within your insurance policy. Most Ontario insurers require you to meet the threshold for "disability," which is a standard that often changes over time. In simple terms, short-term disability is defined as the inability to perform the essential duties of your position due to illness or injury for a period of a few months to a few years. On the other hand, long-term disability refers to such an inability lasting for many years.

Every policy is a contract, and its interpretation is governed by Ontario’s Insurance Act and established case law. This legal framework ensures that ambiguous terms are typically read in favour of the insured person, not the company that wrote the policy. However, insurers frequently rely on narrow interpretations to deny claims. Understanding these definitions, as outlined by sources like the Government of Canada’s guide to the Legal Definitions of Disability, is the first step in protecting your rights. A skilled long term disability lawyer in Brampton can analyze your specific policy wording to build the strongest possible case for your benefits.

Own Occupation vs. Any Occupation

Most long-term disability policies in Ontario feature a significant change in the definition of disability after 24 months. This shift from the "Own Occupation" to the "Any Occupation" standard is a common point where legitimate claims are unfairly terminated. It’s a complex transition that we help clients navigate successfully.

| Feature | "Own Occupation" Period | "Any Occupation" Period |

|---|---|---|

| Typical Timeline | First 24 months of receiving benefits | After 24 months of receiving benefits |

| Definition of Disability | You are unable to perform the essential duties of your own specific job. | You are unable to perform any job for which you are reasonably suited by education, training, or experience. |

| Focus of Assessment | Your ability to do the job you held before you became disabled. | Your transferable skills and capacity for any form of "gainful employment." |

Invisible Disabilities and Mental Health

In the Brampton community, we have seen a substantial increase in disability claims related to mental health since 2020, including for major depressive disorder, anxiety, and PTSD. Insurers are often more skeptical of these "invisible" conditions compared to a physical injury. Proving a claim for chronic pain, fibromyalgia, or a psychological condition requires a robust and strategic approach.

The challenge lies in documenting subjective symptoms with objective evidence. Your personal account of pain or anxiety is vital, but it isn’t enough for an insurer. We work to substantiate your claim with corroborating evidence, such as detailed clinical notes from your psychiatrist or psychologist, records of consistent treatment, reports from vocational experts, and functional capacity evaluations. Understanding how to properly document your condition is a critical step where our legal team provides dedicated guidance, ensuring your insurer cannot unfairly dismiss the severity of your limitations.

Why Insurers Deny LTD Claims: Myths vs. Reality

Receiving a denial letter for your Long-Term Disability (LTD) claim can feel like a final, devastating judgment. It’s a moment filled with anxiety and uncertainty. However, it’s crucial to understand that this is rarely the end of the road. In fact, for many, it’s the point where the real legal process begins. Let’s dismantle the myths and expose the reality behind why insurance companies deny valid claims.

The most pervasive myth is that "if my doctor says I am disabled, the insurance company must pay." While your doctor’s opinion is critical evidence, it doesn’t automatically guarantee approval. The insurance provider makes its decision based on the specific definition of "total disability" outlined in your policy, which can be a very high bar to meet. They are looking for objective medical evidence, such as MRIs, specialist reports, and detailed clinical notes that clearly document your functional limitations. A simple doctor’s note is often not enough.

Insurers frequently deny claims citing "insufficient medical evidence" or "non-compliance with treatment." These reasons can be challenged. An experienced long term disability lawyer brampton understands what insurers look for and can help you and your medical team build a robust file that leaves no room for ambiguity. They may also rely on reports from their own "Independent Medical Examiners" (IMEs), doctors they hire to assess you. While presented as neutral, these reports can be biased, and our legal team knows how to scrutinize them and counter their findings with credible evidence from your own treating specialists.

Common Tactics Used to Terminate Benefits

Insurance companies may employ specific strategies to justify denying or terminating your benefits. They might conduct surveillance, using private investigators or monitoring your social media for any activity they can interpret as inconsistent with your disability. A single photo of you at a family gathering could be used out of context to argue you are not disabled. They also use "transferable skills analyses" to suggest that while you can’t perform your own job, you could work in another sedentary role. A skilled civil litigation lawyer can effectively challenge these tactics in court, exposing their flaws and defending your right to benefits.

Intersection with Other Benefits (CPP-D and WSIB)

Your LTD claim doesn’t exist in a vacuum. It often intersects with government programs, creating layers of complexity. Most LTD policies include an "offset" clause, meaning if you’re approved for Canada Pension Plan Disability (CPP-D) benefits, your insurer can reduce your LTD payment by that amount. If your disability is work-related, an active WSIB claim adds another dimension. If your primary claim is denied, you may need to seek other forms of assistance, and we can advise on how an application to the Ontario Disability Support Program (ODSP) could affect a future appeal. For those on work permits, a disability can also raise questions about your immigration status, a situation where integrated legal advice is essential. A dedicated long term disability lawyer brampton at Nanda & Associate Lawyers can manage these complexities, ensuring all your rights are protected across every platform.

The Process: Appealing a Denial and Filing a Lawsuit

Receiving a denial letter from your insurance company can feel like a final verdict, but it’s often just the beginning of the legal process. The key is to act decisively and strategically. In Ontario, you have a strict deadline: you must file a lawsuit within two years from the date your benefits were first denied or terminated, as mandated by the Limitations Act, 2002. Missing this deadline means losing your right to sue forever.

Many insurers will encourage you to engage in their "internal appeal" process. While it may seem like a reasonable first step, it’s often a strategic delay tactic. The insurer controls this process, it rarely results in a reversal, and it does not pause the two-year limitation period. A seasoned long term disability lawyer Brampton residents trust will often recommend bypassing this internal loop and proceeding directly with a formal lawsuit to protect your rights and apply meaningful pressure on the insurer.

The legal journey, known as litigation, follows a structured path:

-

Statement of Claim: This is the formal document that initiates your lawsuit. We file it with the Ontario Superior Court of Justice and serve it on the insurance company, outlining the facts of your case and the relief you are seeking.

-

Discovery: Both sides exchange all relevant documents. This includes your complete medical file and the insurer’s entire claim file. You will also participate in an Examination for Discovery, where the insurer’s lawyer asks you questions under oath.

-

Mediation: A mandatory step in Ontario where a neutral third-party mediator helps both sides negotiate a resolution.

-

Trial: If a settlement isn’t reached, the case proceeds to trial. However, fewer than 5% of LTD cases ever see a courtroom.

From the date a Statement of Claim is filed, it typically takes between 12 and 24 months to reach a resolution, most often at mediation.

Gathering Evidence in the Peel Region

A successful lawsuit is built on strong, objective evidence. We help our Brampton clients gather crucial medical records from local institutions like Brampton Civic Hospital or the Peel Memorial Centre for Integrated Health and Wellness. Beyond records, we work with your family physician to obtain a detailed "Statement of Opinion" letter. This document goes beyond a diagnosis; it precisely outlines your functional limitations and why they prevent you from working.

The Power of Mandatory Mediation in Ontario

The vast majority of long-term disability claims in Brampton and across Ontario are resolved at mandatory mediation. This confidential meeting brings both parties together with a neutral mediator to facilitate a settlement, which is typically a tax-free, lump-sum payment. At Nanda & Associate Lawyers, we recognize the emotional and financial stress of this day. We provide comprehensive preparation, ensuring you understand the process and feel empowered to make the best decision for your future.

If your LTD benefits have been unfairly denied, don’t let the insurer’s decision be the final word. Contact our experienced team for a consultation to protect your rights and secure the financial stability you deserve.

Practical Advice: Choosing a Long-Term Disability Lawyer in Brampton

Selecting the right legal representation is a critical decision, especially when you are facing the financial and emotional strain of a denied disability claim. The right lawyer doesn’t just understand the law; they understand your situation. Your choice should be based on expertise, accessibility, and a proven track record of fighting for clients’ rights.

Financial concerns are often the most immediate barrier to seeking legal help. That is why we operate on a contingency fee basis. This "No Win, No Fee" promise means you don’t pay any legal fees unless we successfully secure a settlement or judgment for you. This model ensures that everyone has access to justice, regardless of their current income status. It aligns our success directly with yours, providing you with peace of mind to focus on your health.

A serious disability often creates complex, overlapping legal needs. It can impact your family dynamics, your financial future, and your estate plans. This is where a multidisciplinary firm provides a distinct advantage. Instead of seeking separate counsel for different issues, our collaborative team offers comprehensive solutions under one roof. Our personal injury team works alongside experts in family law, real estate, and estate planning to provide a holistic strategy that protects every aspect of your life. This integrated approach is particularly vital in Brampton, where our diverse community deserves accessible and culturally competent legal care. We proudly offer services in over 15 languages to ensure clear communication and genuine understanding for every client we serve.

What to Bring to Your Initial Consultation

To make our first meeting as productive as possible, please bring a few key documents. This allows our team to immediately assess the strength of your case and provide you with clear, actionable advice. Your preparation helps us build a strong foundation for your claim.

-

The Denial Letter: This document outlines the insurer’s specific reasons for denying your benefits.

-

Your Insurance Policy: The full policy or employee benefits booklet contains the definitions and terms that govern your claim.

-

Recent Medical Reports: Any notes, diagnoses, or reports from your family doctor or specialists are crucial evidence.

If your disability has you considering the long-term security of your family, it may be time to consult a wills and estate lawyer in Brampton to ensure your assets and loved ones are protected.

Why Nanda & Associate Lawyers is the Right Choice

With over 20 years of history serving the community, Nanda & Associate Lawyers has built a reputation for diligent advocacy and compassionate client care. The "Associate" in our name represents our core philosophy: a powerhouse of shared legal knowledge. Your case benefits from the collective expertise of our entire team, not just a single lawyer. We understand that litigation is an incredibly stressful process. Our team provides a reassuring, empathetic approach, keeping you informed and supported at every stage.

When you need a long term disability lawyer Brampton residents have trusted for two decades, our firm stands ready to help. We are committed to securing the benefits you are rightfully owed. Don’t let an insurer’s decision compromise your future. Contact us today for a professional consultation and let us fight for the financial stability and peace of mind you deserve.

Your Path Forward: Securing the LTD Benefits You Deserve

Navigating a long-term disability claim denial can feel overwhelming, but you are not out of options. Understanding that the appeal process requires meticulous evidence and that insurers often rely on narrow policy definitions is your first step. The second, and most crucial, is securing expert legal guidance. When you partner with a dedicated long term disability lawyer Brampton residents trust, you significantly improve your chances of a successful outcome.

Since 2003, Nanda & Associate Lawyers has been a steadfast advocate for individuals across Ontario. Our diverse team provides comprehensive legal solutions in over 15 languages, and we operate on a contingency-fee basis for disability claims. This means you don’t pay any legal fees unless we successfully recover your benefits. We believe your focus should be on your health, not on financial stress.

Take control of your situation today. Contact Nanda & Associate Lawyers for a Professional LTD Consultation and let our experienced team fight for you. Your recovery is your priority; let us make your claim ours.

Frequently Asked Questions About Long-Term Disability Claims

How long do I have to sue my insurance company for denying LTD in Ontario?

In Ontario, you generally have two years to sue your insurance company after your LTD claim is denied. This deadline is governed by the Limitations Act, 2002. The two-year clock typically starts on the date you receive a clear and unequivocal denial of your benefits. It’s crucial to act promptly, as missing this deadline can permanently bar you from seeking compensation through legal action. We can help ensure your rights are protected within these strict timelines.

Can I still receive LTD benefits if I am receiving CPP Disability?

Yes, you can receive both LTD and CPP Disability benefits simultaneously. However, almost all long-term disability policies contain an "offset" clause. This means your insurance provider is entitled to reduce your monthly LTD payment by the amount you receive from the Canada Pension Plan (CPP). For example, if your LTD benefit is C$3,000 and you receive C$1,200 from CPP Disability, your insurer will likely only pay you C$1,800.

What is the "Change of Definition" at the two-year mark in LTD policies?

The "Change of Definition" is a critical milestone in most LTD policies, usually occurring after 24 months of receiving benefits. For the first two years, "total disability" is defined as being unable to perform the essential duties of your own occupation. After this point, the definition typically shifts to being unable to perform any occupation for which you are reasonably suited by education, training, or experience. Insurers often use this change to terminate benefits.

Do I have to attend the medical exam requested by the insurance company?

Yes, you are generally required to attend a medical examination, often called an Independent Medical Examination (IME), if your insurer requests one. Your policy contains a cooperation clause that obligates you to participate. Refusing to attend can give the insurance company grounds to terminate your benefits. However, it’s wise to seek legal counsel before the assessment to understand your rights and how to prepare for the appointment.

How much does a long-term disability lawyer cost in Brampton?

Most firms, including ours, handle these cases on a contingency fee basis. This means you don’t pay any legal fees upfront. Your lawyer is paid a percentage of the settlement or award you receive. If we don’t secure a successful outcome for you, you don’t pay legal fees. Finding the right long term disability lawyer in Brampton means finding a team that invests in your success.

Can my employer fire me while I am on long-term disability?

No, your employer cannot fire you simply because you are on disability leave. Doing so would be discriminatory and a violation of Ontario’s Human Rights Code. Your job is protected while you recover. An exception exists if your employment contract becomes "frustrated," meaning there is no reasonable prospect of you ever returning to work in any capacity. This is a complex area of law that requires careful legal assessment.

What happens if my disability is "invisible," like chronic pain or depression?

Invisible disabilities are valid grounds for an LTD claim, and they are quite common. Conditions like fibromyalgia, chronic pain, anxiety, and depression can be just as debilitating as physical injuries. The key to a successful claim is providing strong, consistent, and objective medical evidence from your treating physicians and specialists. This documentation must clearly outline how your symptoms prevent you from working, creating a solid foundation for your case.

Should I follow the internal appeal process provided by the insurance company?

It’s highly recommended you speak with a lawyer before starting an internal appeal. While it seems like the logical first step, these appeals are reviewed by the same insurer that denied your claim and have a very low success rate. Pursuing an internal appeal can also use up valuable time, putting you closer to the two-year deadline to file a lawsuit. Commencing litigation is often a much more effective strategy for securing the benefits you deserve.

{kind=link}

{kind=link}

{kind=link}