In Short:

- Massive Savings: With Bill 114 receiving the Royal Assent on May 12, 2026, Ontario’s enhanced rebate, together with federal tax relief, may now provide up to $130,000 in combined tax relief for eligible new homes.

- Strict Timelines: For buyers relying on Ontario’s expanded 2026 rebate, the Agreement of Purchase and Sale must be signed between April 1, 2026, and March 31, 2027, with primary residences completing construction by Dec 31, 2031.

- Broad Eligibility: The expanded rebate may be available to eligible individual buyers and qualifying rental property purchasers, provided they meet the existing rebate rules and the new timing requirements.

- Closing Hurdles: During the rollout period, some builders may be cautious about applying the enhanced rebate as an upfront credit until administrative forms, guidance, and closing procedures are fully settled.

On May 12, 2026, Ontario’s Bill 114, the HST Relief Implementation Act (Residential Property Rebates), 2026, received Royal Assent. This legislation gives legal effect to Ontario’s temporary HST rebate expansion for eligible new housing transactions. In tandem with federal partnerships, it effectively updates the provincial tax framework to slash the Harmonized Sales Tax (HST) on qualifying newly built homes and residential rental properties across the province.

By providing up to $130,000 in combined tax relief for eligible new homes, this expansion fundamentally transforms the financial landscape for move-up families, buyers, and real estate investors alike. Whether you are eyeing a pre-construction high-rise condo in Toronto, a new townhouse development in Mississauga, or a detached suburban subdivision, understanding how this law functions and involving experienced real estate lawyers from the very beginning is vital to protecting your transaction.

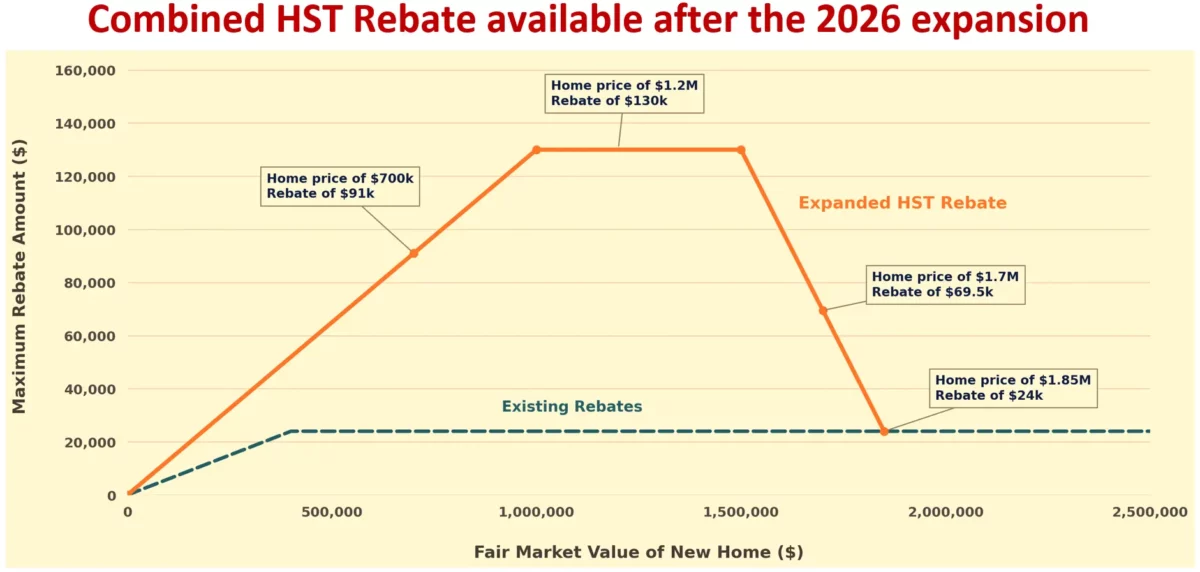

The Rebate Scale: How Much Can You Save?

Under the newly enacted framework, the combination of provincial and federal rebates provides up to $130,000 in joint tax relief for eligible homes. The expansion is governed by a home’s purchase price, breaking down across four specific financial tiers:

- Purchase Price Up to $1,000,000: Qualifying buyers may receive a full 13% HST elimination, wiping out up to $130,000 in total tax liabilities.

- Purchase Price from $1,000,000 to $1,500,000: The rebate hits its maximum plateau, providing tax savings up to $130,000. This tier is particularly crucial for buyers navigating competitive Greater Toronto Area (GTA) pricing structures.

- Purchase Price from $1,500,000 to $1,850,000: The tax relief operates on a sliding linear scale, gradually tapering down from the peak of $130,000 to the historical floor of $24,000.

- Purchase Price Above $1,850,000: The newly expanded brackets phase out completely. However, properties in this premium bracket remain eligible to claim the pre-existing, baseline rebate cap of $24,000.

Strict Eligibility Windows and Construction Deadlines

The expanded HST rebate program is structured as a temporary economic catalyst to stimulate immediate housing supply. To successfully claim the enhanced tax relief, your file must comply with specific statutory dates and construction milestones. Missing these windows will result in the permanent forfeiture of the expanded savings.

- The Agreement Execution Window: For buyers relying on Ontario’s expanded 2026 rebate, the Agreement of Purchase and Sale (APS) between the purchaser and the builder must be signed between April 1, 2026, and March 31, 2027.

- Primary Residence Construction Milestones: For properties purchased with the intent to be used as a primary place of residence, the construction must begin on or before December 31, 2028. Furthermore, the property must reach substantial completion on or before December 31, 2031.

- Residential Rental Property Milestones: For real estate investors claiming the New Residential Rental Property Rebate (NRRPR) variant, the building must reach substantial completion on or before December 31, 2029.

Who Qualifies Under the Law?

A common misconception in the marketplace is that this tax relief is exclusively reserved for first-time homebuyers. The legislation enacted explicitly widens the net, making it accessible to a broader pool of market participants:

- Move-Up Buyers and Downsizers: Existing homeowners, including move-up buyers and downsizers, may qualify where the newly built or substantially renovated home is used as their primary place of residence, or that of a qualifying relation, and all rebate conditions are met.

- Real Estate Investors: The Ontario expansion explicitly integrates the New Residential Rental Property Rebate. Investors may qualify for enhanced rental rebate relief where the property is used for long-term residential rental purposes, and all NRRPR conditions, lease requirements, ownership rules, and construction deadlines are met.

- Property Types: The expanded HST rebate in Ontario generally applies to qualifying new or substantially renovated residential properties, including newly built detached, semi-detached, townhouse, rowhouse, and pre-construction condominium units, provided the buyer meets the applicable rebate rules. Ordinary resale homes are generally HST-exempt, so they do not qualify for this rebate and are not directly affected by the new law.

- Eligibility Requirements: Eligibility depends on the applicable rebate category, ownership structure, intended use, and CRA/Ontario requirements. Buyers should confirm their eligibility before relying on the rebate.

The Closing Reality: The Transitional Period Conflict

While the passage of the HST Relief Implementation Act solidifies the law, the underlying administrative rollout creates immediate procedural challenges for active real estate transactions.

- The Upfront Credit Hurdle: Historically, builders automatically factor the HST rebate into the advertised gross purchase price of a pre-construction unit. The buyer signs a document contractually assigning their rebate rights over to the builder on closing, and in return, the builder reduces the upfront cash required to close the deal.

- Builder Refusals: During the initial rollout period, some builders may be cautious about crediting the enhanced rebate upfront.

- Funding Out-of-Pocket: If a builder cannot or will not credit the enhanced rebate upfront, the buyer must pay the full, unrebated HST out-of-pocket on closing day to secure the title. The buyer must then apply directly to the Canada Revenue Agency after closing to recover the rebate amount. This sudden cash requirement has significant financing impacts, affecting mortgage qualifications and lender calculations at the final hour.

How a Real Estate Lawyer Protects Your Deal

Navigating a real estate transaction during a major legislative shift requires proactive, calculated legal oversight. Partnering with an experienced legal team ensures your asset is secure:

- Ironclad Statement of Adjustments Audits: We meticulously scrutinize your builder’s final statement of adjustments to verify exactly how your rebate allocation is calculated and ensure the builder is not applying hidden administrative offsets.

- Enforcing Protective Contract Clauses: Initially, some builders may be hesitant about crediting the enhanced rebate upfront. In such cases, we help buyers understand potential closing costs and financing implications. We review and negotiate contract language aimed at protecting your rebate position where construction or completion deadlines are relevant.

- Precision Post-Closing CRA Filings: If the rebate is not credited upfront, we assist with post-closing rebate applications and supporting documents to help reduce filing errors and delays.

Maximize your transaction safety during this unprecedented tax shift by securing trusted legal representation early. From analyzing complex pre-construction contract windows to managing transitional CRA refund applications, our dedicated team provides the comprehensive oversight your equity deserves. Reach out to Nanda & Associate Lawyers today to lock in your closing review and protect your property investment.

{kind=link}

{kind=link}

{kind=link}