Receiving a legal notice threatening your home is a deeply unsettling experience. For homeowners in Mississauga, the prospect of a power of sale can be particularly daunting, creating immense stress and confusion over complex timelines and unfamiliar legal terms. The fear of losing your primary residence, coupled with uncertainty about your rights and options, can feel overwhelming. Many are left wondering what the process truly entails and how it differs from a foreclosure.

This comprehensive legal guide is designed to provide clarity and restore your sense of control. We will demystify the power of sale process in Ontario, offering the expert insights you need to make informed decisions in 2026. Within this article, you will learn how to navigate the legal notices, understand your options for stopping the sale through redemption or refinancing, and ensure your rights are protected. Our goal is to equip you with the knowledge to safeguard your home, preserve your hard-earned equity, and face this challenge with confidence.

Key Takeaways

- Learn proactive strategies, including lender negotiation and refinancing options, to potentially stop a power of sale and secure your property in Mississauga.

- Understand the critical legal timeline, from the initial default notice to the final sale, so you can act decisively to protect your home.

- Discover the key difference between a power of sale and foreclosure, particularly how each process affects your right to surplus equity.

- Recognize how professional legal representation can ensure lender compliance with the Mortgages Act and strengthen your negotiating position.

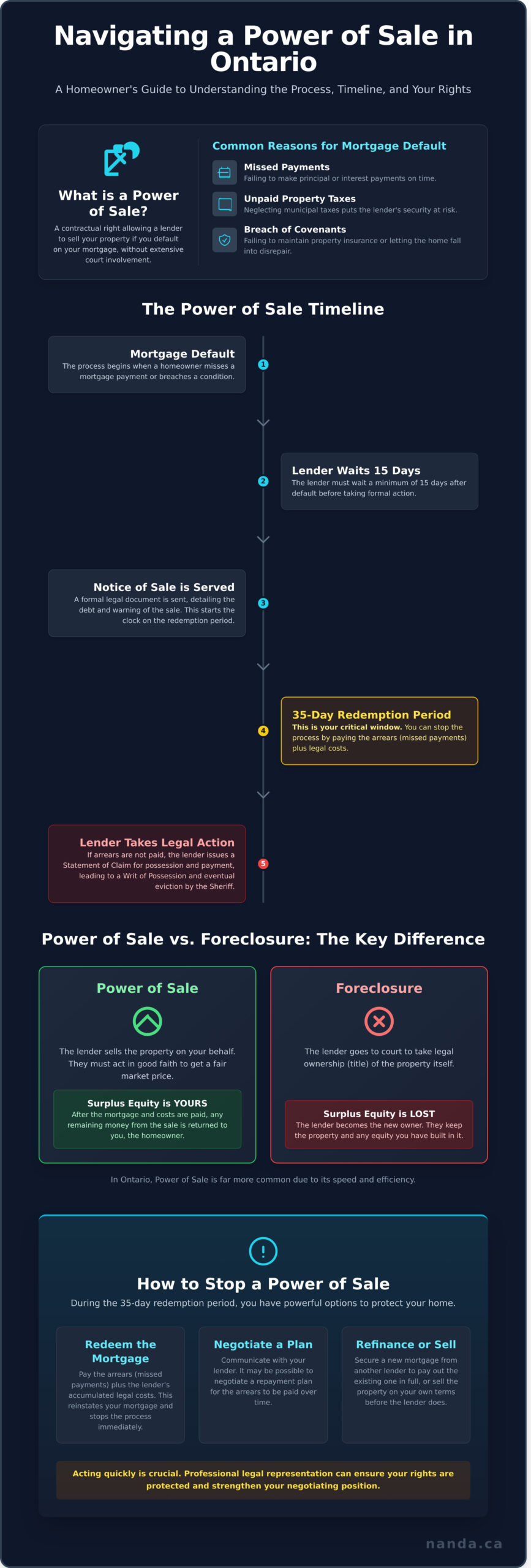

What is a Power of Sale in Ontario Real Estate?

When a homeowner defaults on their mortgage, the lender has several legal remedies available to recover their investment. In Ontario, the most common and efficient of these is the power of sale. This is a provision written directly into most mortgage contracts that gives the lender (the mortgagee) the right to sell the property if the borrower (the mortgagor) fails to meet their obligations. This process is governed by the Mortgages Act of Ontario, which provides a clear and enduring framework for these proceedings, ensuring its relevance well into 2026 and beyond.

Lenders in Mississauga and across the province generally prefer this route over the alternative, foreclosure. The primary distinction is that a power of sale is a contractual remedy that does not require extensive court involvement, making it faster and less costly. Foreclosure, on the other hand, is a more complex judicial process where the lender sues the borrower to take ownership of the property. For a detailed overview of this alternative process, you can learn more about what is foreclosure and how it differs significantly from the contractual rights exercised in a power of sale. Ultimately, the lender sells the property, pays off the mortgage debt and associated costs, and returns any surplus funds to the homeowner.

Common Reasons for Mortgage Default in Mississauga

A mortgage default can be triggered by more than just missed payments. While failing to pay principal and interest is the most frequent cause, a homeowner can also be in default for breaching other important terms of their mortgage agreement, known as covenants. Common reasons include:

- Failure to make principal or interest payments on time.

- Neglecting to pay property taxes to the City of Mississauga, which can place the lender’s security at risk.

- Failing to maintain adequate property insurance or allowing the property to fall into a state of disrepair.

The Legal Participants in the Process

Navigating a power of sale involves several key parties, each with specific rights and duties. The Mortgagor is the homeowner, who retains certain rights, including the right to bring the mortgage back into good standing before a sale. The Mortgagee is the lender, who has a fiduciary duty to act in good faith, sell the property for a fair market value, and account for all proceeds. Other parties, such as guarantors who co-signed the loan and secondary lien holders (e.g., a second mortgage lender), are also involved and have a right to be notified of the proceedings.

The Power of Sale Timeline: From Default to Eviction

Navigating a power of sale can be an intimidating experience, but it is essential to understand that it is a structured legal process governed by strict timelines. It does not happen overnight. The process begins after a homeowner defaults on their mortgage, typically by missing a payment. The lender must then wait a minimum of 15 days before they can take formal action, providing a brief initial window to address the issue.

Understanding the Notice of Sale

After the 15-day default period, the lender will formally serve a Notice of Sale Under Mortgage, often called the “Red Notice.” This is a critical legal document. To be valid, the notice must be served via prepaid registered mail and contain specific details, including the mortgage date, the total amount currently due (including principal, interest, and any associated costs), and a clear warning that the property will be sold if the arrears are not paid. These requirements are strictly outlined in Ontario’s Mortgages Act. Any errors or omissions in this notice can render it invalid and stall the entire process, making a professional legal review imperative.

The Redemption Period: Your Window for Action

Once the Notice of Sale is served, a 35-day period known as the redemption period begins. This is a crucial timeline that provides the homeowner with a protected window to take action. During these 35 days, the homeowner has the right to redeem the mortgage by paying only the arrears-the missed payments plus the lender’s legal costs-to bring the mortgage back into good standing. The lender cannot demand the full mortgage balance at this stage and is legally prohibited from selling or even listing the property for sale until this period expires.

If the redemption period ends without payment, the lender can proceed by issuing a Statement of Claim to obtain a court order for both possession of the property and payment of the debt. If successful, the court issues a Writ of Possession. This final document is delivered to the local Sheriff-for example, the Sheriff of Peel in Mississauga-who is then authorized to schedule and enforce the eviction, transferring control of the property to the lender.

Power of Sale vs. Foreclosure: Key Differences for Homeowners

While the terms are often used interchangeably, the legal and financial outcomes for an Ontario homeowner are vastly different. Understanding the core distinctions in the Power of Sale vs. Foreclosure debate is the first step toward protecting your interests when facing mortgage default. In Ontario, the vast majority of lenders utilize the power of sale clause embedded in most mortgage agreements.

The fundamental differences can be summarized as follows:

- Ownership Status: During a power of sale, you legally retain ownership (the title) of your property until it is officially sold to a new buyer. In a foreclosure, the lender applies to the court to take the title and become the owner themselves.

- The Right to Surplus: This is the most critical distinction. After a power of sale, any funds remaining after the mortgage, legal fees, and other secured debts are paid belong to you, the homeowner. In a strict foreclosure, the lender keeps the property and all the equity it contains.

- Speed of Process: A power of sale is a faster and more cost-effective contractual remedy for the lender. A foreclosure is a more complex and lengthy court action, which is why it is far less common in Ontario.

- Deficiency Judgments: In either process, if the sale proceeds are insufficient to cover the total debt owed, the lender can sue you personally for the shortfall.

What Happens to Your Equity?

Under a power of sale, the lender has a legal duty to act in good faith and sell the property for fair market value. They cannot simply accept a low offer to expedite the process. For instance, in a competitive market like Mississauga, this means taking reasonable steps to secure a price comparable to similar local homes. If the sale generates a surplus, these funds are used to pay any secondary mortgage holders or lienholders, with the final balance returned to you. Should you believe the lender sold your home improvidently, you may have legal grounds to challenge the sale.

Foreclosure: The Rarer Alternative

A lender might pursue foreclosure if there is substantial equity in the home that they wish to obtain for themselves. This judicial process requires them to go to court to extinguish your ownership rights and your right to the equity. However, as the homeowner, you are not without recourse. You can request that the court convert the foreclosure into a judicial sale, which compels the property to be sold under court supervision. This action effectively protects your right to receive any surplus equity, similar to a power of sale.

How to Stop a Power of Sale in Mississauga

Receiving a Notice of Sale Under Mortgage is a deeply stressful experience, but it is not the final word. Homeowners in Mississauga and the Peel Region have several strategic options to stop a power of sale and regain control of their financial future. Taking swift, decisive action is paramount, as the options available narrow with time. We recommend exploring these avenues with the guidance of an experienced legal professional.

Your primary strategies for halting the process include:

- Negotiating with the Lender: Immediate and transparent communication is your first line of defense. Lenders are often willing to negotiate a repayment plan or other arrangements, as the legal process is costly for them as well.

- The Right to Reinstate: Under Ontario law, you have the right to “reinstate” your mortgage by paying all arrears, including missed payments, interest, and the lender’s legal and administrative costs. This payment stops the clock on the sale process.

- Refinancing the Mortgage: If your primary lender is unwilling to negotiate, you may be able to secure a new mortgage from a B-lender or a private lender to pay out the existing one.

- Selling the Property Privately: You retain the right to sell your home on your own terms until the lender takes possession. This allows you to control the sale price and process, potentially preserving more of your home equity than a lender’s sale would.

Legal Defenses and Court Injunctions

In certain circumstances, a court may grant an injunction to stay the sale. This typically occurs if the lender has made a significant procedural error, such as providing improper notice or miscalculating the amount owed. A Mississauga real estate lawyer can meticulously review your file to identify such errors and, if found, represent you in court to halt the power of sale proceedings while the issues are litigated and resolved.

Refinancing and Private Lending Solutions

For homeowners with sufficient equity, refinancing through a private lender can provide the emergency funding needed to pay out the mortgage in default. While these loans carry higher interest rates, they offer a crucial lifeline. A successful private mortgage requires a solid exit strategy-a clear plan to either return to a traditional lender or sell the property on your terms-to avoid facing a second default when the short-term loan comes due.

Navigating these complexities requires a skilled legal partner. At Nanda & Associate Lawyers Professional Corporation, we provide the comprehensive legal solutions needed to protect your home and your interests. For a confidential consultation, we invite you to contact our team today.

Why Legal Representation is Essential for Power of Sale Matters

Facing a power of sale can be an overwhelming and isolating experience. The legal notices, strict deadlines, and financial pressures often leave homeowners feeling powerless. However, securing experienced legal representation is the single most important step you can take to protect your rights, your property, and your financial future. An experienced lawyer does more than just explain the process; they become your strategic advocate.

A skilled legal team will meticulously review all documents from the lender to ensure they have strictly complied with the procedural requirements of Ontario’s Mortgages Act. Any misstep by the lender could provide crucial leverage. We also engage in strategic negotiation on your behalf, aiming to extend timelines to give you more options, or to reduce exorbitant legal fees added to your mortgage debt. Our goal is to mitigate the financial damage and create the best possible outcome from a difficult situation, safeguarding your credit score and long-term stability.

The Nanda Advantage in Mississauga

At Nanda & Associate Lawyers, we combine decades of experience in Ontario real estate law with a robust civil litigation practice. This dual expertise is critical for effectively managing power of sale cases. Our diverse, multilingual team ensures you understand every detail of your legal position in the language you are most comfortable with. We use a collaborative team approach to develop the comprehensive legal solutions needed to navigate these complex challenges with confidence.

Next Steps: Securing Your Consultation

Taking decisive action is key. When you meet with our team, we ask that you bring all relevant documents to help us conduct a thorough assessment. This includes:

- The original mortgage agreement

- Any Notices of Sale or other correspondence from the lender

- A recent mortgage statement showing the amount in arrears

During this initial meeting, we will assess the validity of the lender’s claims and outline a clear, strategic path forward for your specific circumstances. Don’t face this challenge alone. Contact Nanda & Associate Lawyers today for a confidential consultation.

Navigating Power of Sale with Confidence and Clarity

Understanding the Ontario power of sale process is the first critical step toward protecting your property and financial future. This guide has shown that while the timeline is strict, homeowners have defined rights and strategic options available to them. The most crucial takeaway is that you do not have to face this complex legal challenge alone; timely, professional intervention is your strongest asset.

Since 2003, Nanda & Associate Lawyers has provided comprehensive legal solutions to the Mississauga community and across Ontario. Our firm’s unique strength lies in our combined expertise in both Real Estate Law and Civil Litigation, ensuring we can protect your interests from every angle. With a dedicated, multilingual team fluent in over 15 languages, we deliver clear, culturally sensitive, and decisive legal counsel.

Do not let uncertainty dictate your next steps. Take control of the situation today. Speak with a Mississauga Real Estate Lawyer Now to secure the peace of mind that comes with having a powerful advocate on your side.

Frequently Asked Questions About Power of Sale

Can I stop a power of sale after the 35-day redemption period has passed?

While challenging, it is not always impossible. After the redemption period expires, the lender can enter into a binding Agreement of Purchase and Sale. Once this agreement is signed, your right to redeem the mortgage is typically lost. However, if no such agreement is in place, you may still have a window of opportunity. Immediate legal action is essential to determine if any options remain to halt the process and protect your property.

Does a power of sale stay on my credit report in Ontario?

Yes, a power of sale has a severe and long-lasting negative impact on your credit report. Lenders will report the mortgage default to credit bureaus, resulting in an R9 rating-the lowest possible score. This serious delinquency will remain on your credit history for approximately seven years from the date of the last activity, making it extremely difficult to obtain future mortgages, loans, or other forms of credit at competitive rates.

What is the lender’s “Duty of Care” when selling my property?

In Ontario, a lender exercising a power of sale has a legal duty to act in a commercially reasonable manner to secure the best possible price for the property under the prevailing market conditions. This typically involves listing the property on MLS, obtaining appraisals, and ensuring it is exposed to the market. They cannot simply sell it for the outstanding mortgage balance if its fair market value is higher. Failure to meet this standard may give you grounds for legal recourse.

How much are the legal fees usually charged by the lender in a power of sale?

The lender’s legal fees are added to the total debt you owe. These costs can vary significantly based on the complexity of the case but often range from C$2,500 to C$5,000 or more, especially if court proceedings become necessary. These fees, along with real estate commissions, property management, and appraisal costs, are all deducted from the sale proceeds before any remaining funds are returned to you. You are ultimately responsible for all these expenses.

Can I still live in my house during the power of sale process?

You have the right to occupy your home during the initial stages, including the redemption period. However, once the lender sells the property and needs to provide vacant possession to the new buyer, they will take legal steps to have you removed. This usually involves obtaining a Writ of Possession from the court. It is advisable to cooperate with this process to avoid the added cost and stress of a forced removal by the Sheriff.

What happens if the house sells for less than what I owe the bank?

If the sale proceeds are insufficient to cover the mortgage balance, legal fees, and all other associated costs, the shortfall is known as a “deficiency.” The lender has the legal right to pursue you personally for this remaining amount. They can initiate a lawsuit to obtain a judgment against you, which may lead to actions such as wage garnishment or placing liens on any other assets you own until the debt is fully paid.

Is a power of sale the same as an eviction notice in Mississauga?

No, they are distinct legal concepts. A power of sale is the lender’s contractual right to sell your property due to mortgage default. An eviction notice is typically used in a landlord-tenant relationship. However, as part of the power of sale process, if you do not vacate the property after it is sold, the lender or the new owner will need to obtain a court order for possession, which effectively serves to evict you from the home.

Can I sell my own house if the bank has already started the power of sale?

Yes, you retain the right to sell your property yourself, but you must act with urgency. Your ability to sell is only available until the lender signs a binding Agreement of Purchase and Sale with another buyer. Selling the home yourself allows you to control the process, potentially achieve a higher price, and use the proceeds to pay off the mortgage arrears, legal costs, and principal in full, thereby stopping the lender’s action and protecting your equity.

{kind=link}

{kind=link}

{kind=link}