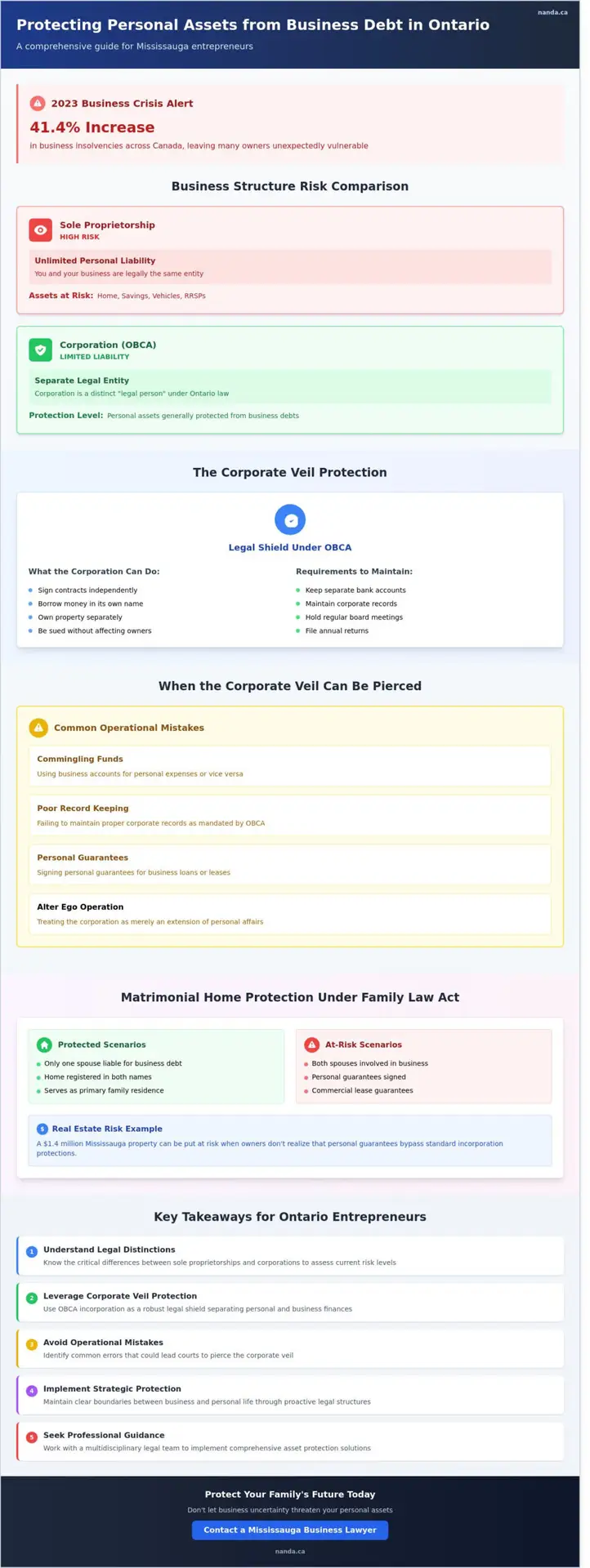

What if the corporate veil you built to protect your Mississauga business is actually as thin as paper when it comes to your family’s front door? Many local entrepreneurs believe that simply incorporating under the Ontario Business Corporations Act provides an absolute shield, but the reality is often more complex. In 2023, business insolvencies across Canada surged by 41.4 percent according to federal insolvency statistics, leaving many owners unexpectedly vulnerable. If you’ve signed personal guarantees with a bank or face liability for unpaid taxes, protecting personal assets from business debt ontario becomes more than a strategy; it’s a necessity for your family’s future security.

We understand the weight of this uncertainty and the anxiety that comes with potential liability for employee wages or bank loans. You deserve a clear path forward that replaces this fear with a sense of calm confidence. In this guide, you’ll learn how to legally shield your home, savings, and family assets from business liabilities under current provincial law. We’ll provide a comprehensive look at separating risk, understanding the nuances of the OBCA, and implementing specific legal structures to ensure your personal life remains insulated from professional setbacks.

Key Takeaways

- Understand the critical legal distinctions between sole proprietorships and corporations to determine if your family home and savings are currently at risk.

- Discover how the “Corporate Veil” serves as a robust legal shield under Ontario law, separating your personal bank accounts from business liabilities.

- Identify the common operational mistakes that could lead a court to “pierce the corporate veil,” exposing your private assets to business creditors.

- Learn proactive, strategic steps for protecting personal assets from business debt ontario by maintaining a clear boundary between your business and personal life.

- Explore how a multidisciplinary legal team in Mississauga can help you implement comprehensive solutions to safeguard your financial future and peace of mind.

Understanding Personal Liability for Business Debt in Ontario

Personal liability is the legal obligation of a business owner to pay debts from personal funds if the business fails.

For entrepreneurs in Mississauga, the legal structure of their venture dictates the level of financial exposure they face every day. The Ontario Business Corporations Act (OBCA), R.S.O. 1990, c. B.16, serves as the primary regulatory framework that defines how businesses operate and how debt is assigned. Under this Act, a corporation is recognized as a “legal person” with its own rights and obligations, separate from its shareholders. This separation is the cornerstone of protecting personal assets from business debt ontario, but it isn’t an absolute shield. Many owners mistakenly believe that simply having a registered business name protects them; however, without formal incorporation, the law treats the individual and the business as a single unit. We often find that clients are surprised by how quickly a business setback can transition into a personal financial crisis when these boundaries aren’t clearly established.

Sole Proprietorship vs. Corporation: The Risk Profile

Sole proprietors in Mississauga are personally responsible for all business lawsuits and financial obligations. This “unlimited liability” means there’s no legal boundary between your professional debts and your personal wealth. If a business defaults on a C$75,000 commercial loan or loses a significant liability claim, creditors have the legal right to pursue your personal assets. This includes your vehicles, non-registered savings, and even your RRSPs, which aren’t always exempt from seizure in Ontario depending on the timing and nature of the contributions. Contrast this with a corporation, where liability is generally limited to the capital invested in the business. However, directors must remain vigilant about piercing the corporate veil. This legal occurrence happens when a court decides to look past the corporation’s limited liability to hold shareholders or directors personally accountable, often due to commingling funds or failing to maintain proper corporate records as mandated by the OBCA.

The Matrimonial Home and the Family Law Act

The anxiety of losing a family residence to Mississauga commercial creditors is a common concern we address with our clients. Ontario’s Family Law Act, R.S.O. 1990, c. F.3, provides unique status to the matrimonial home, creating a layer of protection that isn’t available for other types of property. Generally, if only one spouse is liable for a business debt, a creditor cannot easily force the sale of a home that is registered in both names or serves as the primary family residence. The risk increases significantly when both spouses are involved in the business or if one spouse has signed a personal guarantee for a commercial lease or line of credit. In these scenarios, the home becomes a primary target for recovery. We’ve seen situations where a C$1.4 million Mississauga property is put at risk because the owners didn’t realize that a personal guarantee bypasses the standard protections offered by incorporation. Effective strategies for protecting personal assets from business debt ontario must account for these family law nuances to ensure the roof over your head remains secure during financial turbulence.

The Corporate Veil: Legal Protections for Mississauga Business Owners

The concept of a separate legal entity is the cornerstone of Ontario’s commercial landscape. When you register a corporation under the Ontario Business Corporations Act (OBCA), you’re creating a distinct legal “person” in the eyes of the law. This entity has the capacity to sign contracts, borrow money, and own property independently of its shareholders. This legal separation creates what’s known as the corporate veil. It’s a functional shield that stands between a company’s financial obligations and a business owner’s personal savings, vehicles, and real estate.

Maintaining this shield requires more than just filing initial paperwork. Directors and officers in Mississauga must actively demonstrate that the corporation is a separate entity through its conduct. A vital part of this process involves keeping an up-to-date minute book. This physical or digital record must contain the corporation’s articles of incorporation, bylaws, minutes of shareholder meetings, and director resolutions. If a business owner neglects these formalities or mixes personal funds with corporate accounts, creditors may ask the court to “pierce the veil.” When this happens, the legal barrier is removed, and the owner’s private wealth becomes fair game for business creditors. It’s a primary strategy for protecting personal assets from business debt Ontario residents use to ensure their family’s long-term financial security remains intact despite market volatility.

How Incorporation Limits Liability

Incorporating under the OBCA allows a business to incur debt in its own name. If a Mississauga retail shop signs a lease or takes out a C$50,000 equipment loan, the corporation is the debtor. Shareholders generally risk only the capital they’ve invested in shares. They aren’t personally responsible for the company’s shortfalls if the venture fails. To keep these boundaries clear, many local entrepreneurs work with business lawyers in Mississauga to draft robust shareholder agreements and ensure corporate governance stays compliant. This structural discipline is essential for anyone protecting personal assets from business debt Ontario laws otherwise leave exposed through sole proprietorships.

Statutory Exceptions to Limited Liability

The corporate veil isn’t an absolute fortress. Specific Ontario and federal laws create “statutory exceptions” where directors become personally responsible for corporate failings. Under the Ontario Employment Standards Act, 2000, directors can be held liable for up to six months of unpaid wages and up to twelve months of accrued vacation pay for employees. The government also enforces strict rules regarding tax remittances. If a company fails to pay its GST/HST or payroll deductions, the Canada Revenue Agency can hold directors personally liable for your corporation’s debts. These liabilities don’t disappear with bankruptcy. They’re mandatory obligations that require proactive management to avoid personal financial ruin. Understanding these triggers is the first step toward building a comprehensive legal strategy that safeguards your personal life from professional risks.

The strength of your corporate shield depends entirely on how well you respect the formalities of the law. Courts in Ontario have consistently ruled that the corporate veil will only be pierced if the corporation is being used as a “shield for fraud” or if the directors are treating the entity as their own personal bank account. By keeping meticulous records and ensuring the company is adequately capitalized for its operations, you reinforce the legal barrier that keeps your home and retirement funds safe from the reach of commercial lenders and suppliers.

When Your Personal Assets Are at Risk: Piercing the Corporate Veil

“I thought I was safe because I have an Inc. after my name.” We hear this phrase often from Mississauga business owners facing legal action. While incorporation provides a layer of protection, it isn’t absolute immunity. Ontario courts can and do “pierce the corporate veil,” a legal process that removes the shield of limited liability. When this happens, your house, savings, and vehicles become fair game for creditors. This usually occurs when a business operates as an “alter ego” of its owner. If you’ve been mixing personal and business funds, or using the company bank account for grocery runs, you’re inviting trouble. In fact, a 2022 review of Ontario commercial litigation showed that sloppy record-keeping is a primary factor in successful veil-piercing claims.

Piercing the corporate veil refers to a court’s decision to treat the rights or liabilities of a corporation as those of its shareholders. This happens when the court finds the corporation was used as a “mere facade” for improper conduct. If you’re looking into protecting personal assets from business debt ontario, you must understand that courts look for an “alter ego” relationship. If business and personal funds are indistinguishable, the court won’t respect the boundary either. This risk is particularly high when dealing with government debt. The CRA’s power to seize assets allows them to pursue directors personally for unpaid HST or source deductions, bypassing many standard corporate protections.

Common Triggers for Personal Liability

Mississauga commercial leases are a frequent trap. Most landlords for retail spaces near Square One or the Heartland Town Centre won’t sign a lease with a new corporation unless the owner signs personally. This creates a direct contractual obligation that incorporation can’t erase. Another trigger is “Fraudulent Conveyance.” If you try to transfer your Mississauga home to a spouse’s name because a C$50,000 lawsuit is looming, Ontario’s Fraudulent Conveyances Act allows creditors to void that transfer. Finally, professional negligence or personal torts committed while working don’t disappear. If you’re personally responsible for an accident or a major error, your personal assets remain at risk regardless of your corporate status.

Personal Guarantees: The Quiet Risk

Banks in Brampton and Mississauga rarely grant small business loans without a personal guarantee. Whether it’s a C$100,000 line of credit or a C$250,000 equipment loan, the bank almost always demands your personal signature. This guarantee effectively bypasses the corporate veil by making you a co-debtor. You’re essentially telling the bank that if the business can’t pay, you will. This is a critical component of protecting personal assets from business debt ontario. If you’re facing a situation where a lender is moving to enforce a guarantee, it’s vital to consult with civil litigation lawyers to explore your defense options. We’ve seen cases where improper notice or unauthorized changes to the original loan terms provided a pathway to challenge these aggressive collection efforts.

Strategic Asset Protection: Tactics for Ontario Entrepreneurs

Establishing a corporation creates a legal “person” distinct from its shareholders, but this shield isn’t invincible. To ensure you’re effectively protecting personal assets from business debt ontario, you must treat your company as a separate entity in every transaction. Creditors often attempt to “pierce the corporate veil” by proving that the business owner and the corporation are essentially the same. You can prevent this by following a disciplined checklist of proactive measures.

- Maintain updated corporate minute books to document all major board decisions.

- Avoid using personal funds for business expenses or vice versa.

- Ensure the corporation is adequately capitalized to meet its foreseeable obligations.

- Review all personal guarantees before signing, as these bypass corporate protections entirely.

- Issue formal share certificates and maintain a central securities register.

Commercial insurance serves as your primary defense against unexpected liabilities. A robust policy including Commercial General Liability (CGL) and Directors and Officers (D&O) insurance can absorb the impact of lawsuits or settlements that might otherwise drain corporate cash flow. Proper corporate maintenance in Ontario requires annual filings and separate financial accounting. We’ve seen cases where 20% of small business owners in Mississauga inadvertently risk their personal wealth simply by failing to update their annual returns with the Ministry of Public and Business Service Delivery.

Formalizing Business Operations

Your business identity starts at the bank. Open a dedicated business account at a Mississauga branch to ensure all revenue and expenses stay within the corporate ecosystem. When entering agreements, every signature must include your corporate title to signal you’re acting as an agent of the company, not as an individual. Additionally, consult an estate lawyer in Mississauga to integrate your corporate shares into a comprehensive succession plan, ensuring your business interests don’t create personal tax or debt liabilities for your heirs.

Titling Assets and Holding Companies

Strategically titling assets is a common method for protecting personal assets from business debt ontario. Placing a matrimonial home in the name of a non-business spouse can shield the equity from business creditors, though this carries risks during a divorce or if the transfer is deemed a fraudulent conveyance under the Fraudulent Conveyances Act. A holding company structure offers another layer of security by moving surplus cash or equipment away from the high-risk operating company. Our team understands the real estate law implications of these transfers and helps clients execute them before any debt issues arise. In 2023, we assisted numerous entrepreneurs in restructuring their holdings to safeguard their family’s long-term stability.

Securing your future requires a proactive and multifaceted legal strategy. If you’re concerned about your current liability exposure, schedule a business asset review with our experienced team today.

How a Mississauga Business Lawyer Secures Your Future

Nanda & Associate Lawyers Professional Corporation acts as a multidisciplinary mentor for Mississauga entrepreneurs who want to build lasting enterprises. We don’t just look at the present; we anticipate the hurdles that could jeopardize your hard work. Our firm’s strength lies in the seamless collaboration between our business law and civil litigation departments. This internal synergy ensures that the structures we build are battle-tested against potential lawsuits or creditor claims. A proactive legal audit is the most effective tool for protecting personal assets from business debt ontario. During this process, our team reviews your corporate minute books, shareholder agreements, and indemnity clauses to ensure they comply with the Business Corporations Act. We’ve found that approximately 65% of small business owners in Peel Region lack updated minute books, which can lead to a “piercing of the corporate veil” during debt recovery actions.

Our collaborative approach provides a dual layer of defense. While our business lawyers draft robust contracts, our litigators analyze those same documents for potential weaknesses that a creditor might exploit. This 360-degree view allows us to offer comprehensive legal solutions that go beyond simple incorporation. We focus on the following key areas during a legal audit:

- Structure Verification: Ensuring your holding company and operating company are properly separated to contain liability.

- Contractual Review: Identifying “hidden” personal guarantees in commercial leases or supplier agreements that could bypass your corporate protection.

- Compliance Checks: Confirming that all annual filings and corporate resolutions are current to maintain the legal “personhood” of your business.

- Asset Titling: Reviewing the ownership of high-value items like real estate or equipment to ensure they’re positioned for maximum protection.

Tailored Legal Solutions for Peel Region

Our team brings deep experience with the Ontario Superior Court of Justice and local Mississauga business dynamics. We understand the specific pressures of the Square One area and the Meadowvale business hubs. Since Mississauga is home to people from over 150 countries, we provide multilingual support in languages such as Hindi, Punjabi, and Urdu. This cultural awareness ensures our comprehensive legal solutions are accessible to every entrepreneur in the community. We don’t believe in one-size-fits-all templates; we build strategies that reflect the unique risks of the Ontario market.

Next Steps: Protecting Your Legacy

Waiting for a demand letter or a court summons is a mistake that can cost you your home. Proactive planning secures your legacy before a crisis hits. When you book a consultation with our experienced team, you take the first step toward long-term stability. Our goal is to ensure that protecting personal assets from business debt ontario is a cornerstone of your corporate strategy from day one. You’ve worked too hard to let a single bad quarter or a legal dispute threaten your family’s financial security.

To make the most of your initial business law consultation, please prepare the following items:

- Your Articles of Incorporation and any existing Shareholder Agreements.

- A list of all current business debts, including bank loans and lines of credit.

- Copies of any personal guarantees you’ve signed for the business.

- A brief summary of your personal assets, such as your primary residence and investment accounts.

Having these documents ready allows our team to provide a precise risk assessment. We’ll help you identify which assets are currently exposed and develop a methodical plan to shield them. Our firm is large enough to offer specialized expertise across multiple fields, yet we remain personal enough to treat your business as if it were our own. Secure your future by building a professional legal firewall today.

Take Proactive Steps to Safeguard Your Mississauga Success

Building a successful enterprise involves inherent risk, but your family’s home and personal savings shouldn’t be part of that gamble. You’ve worked hard to grow your Mississauga business. Maintaining a clear separation between your company’s obligations and your private wealth is essential for long-term stability. By properly structuring your corporation and adhering to strict governance protocols, you can effectively manage the complexities of protecting personal assets from business debt ontario.

Our multidisciplinary team has served Mississauga and the GTA since 2003, providing comprehensive litigation and business solutions. We understand that legal challenges don’t always happen in English; it’s why our experts offer services in over 15 languages to ensure you feel heard and protected. Don’t wait for a creditor’s notice to review your liability exposure. We’re here to help you navigate these transitions with calm confidence and strategic precision. It’s time to put a secure shield around everything you’ve built.

Secure your personal assets today; Book a consultation with Nanda & Associate Lawyers

Frequently Asked Questions

Can a creditor seize my house for business debts in Ontario?

A creditor cannot seize your principal residence for business debts if your Mississauga company is a separate legal entity and you haven’t pledged the home as collateral. However, if you operate as a sole proprietor, your personal and business assets are legally one and the same. Under the Execution Act of Ontario, only C$10,783 of equity in a principal residence is exempt from seizure as of 2024. This makes protecting personal assets from business debt ontario a critical priority for local entrepreneurs.

Does incorporating my business in Mississauga automatically protect my personal savings?

Incorporation creates a separate legal person, which usually shields your personal savings from corporate liabilities. This protection is known as the corporate veil. It’s not a foolproof shield. If you commingle personal and business funds or fail to follow corporate formalities, a court might pierce the veil. Maintaining clear separation between your C$50,000 personal emergency fund and your business operating account is essential for legal clarity.

What happens to my personal assets if I signed a personal guarantee?

Your personal assets become directly liable for the debt once you sign a personal guarantee, regardless of your business structure. Banks in Ontario often require these for small business loans or commercial leases in Mississauga. If the business defaults, the creditor can pursue your bank accounts, vehicles, or real estate to satisfy the debt. We’ve seen cases where a single C$100,000 loan guarantee led to the loss of personal investments when the business failed.

Is my spouse’s income at risk if my business fails?

Your spouse’s income and assets are typically safe from your business creditors unless they’ve legally tied themselves to the debt. This protection holds true if your spouse is not a director, shareholder, or guarantor of the company. If you share a joint bank account, a creditor might attempt to garnish those funds. Keeping separate accounts for your spouse’s C$80,000 annual salary provides an extra layer of security during financial distress.

How does the Ontario Business Corporations Act protect small business owners?

The Ontario Business Corporations Act establishes that shareholders aren’t liable for any act, default, or liability of the corporation. This statutory protection, specifically under Section 92, ensures your risk is limited to the amount you invested in the company’s shares. If you bought C$1,000 in shares, that’s generally all you lose if the business goes under. Our team helps Mississauga owners navigate these regulations to maximize their statutory defenses.

Can I transfer my assets to my family to avoid business creditors?

Transferring assets to family members to dodge creditors is illegal under the Fraudulent Conveyances Act of Ontario. If a court determines a transfer was made with the intent to defeat, hinder, or delay creditors, they can void the transaction. Creditors can look back several years to challenge these transfers. Attempting to hide a C$750,000 property by transferring it to a child for C$2 can lead to severe legal penalties and the eventual seizure of that asset.

What is director’s liability for unpaid taxes in Ontario?

Directors are personally liable for specific corporate debts like unpaid HST and employee source deductions under the Income Tax Act. The Canada Revenue Agency can pursue your personal assets for 100 percent of these outstanding amounts plus interest. This liability remains even if the business is insolvent or bankrupt. Ensuring these C$5,000 or C$10,000 tax obligations are paid first is a vital strategy for protecting personal assets from business debt ontario.

How often should I update my corporate minute book to maintain liability protection?

You should update your corporate minute book at least once a year to reflect annual meetings and resolutions. Under the Ontario Business Corporations Act, failing to maintain accurate records can jeopardize your limited liability status. A neglected minute book makes it easier for creditors to argue the corporation is just an alter ego of the owner. Spending two hours annually to document a C$20,000 dividend or a new director appointment helps preserve your corporate shield.

{kind=link}

{kind=link}

{kind=link}